Cash flow modelling, we believe, is the integral part of any serious client centred financial planning process.

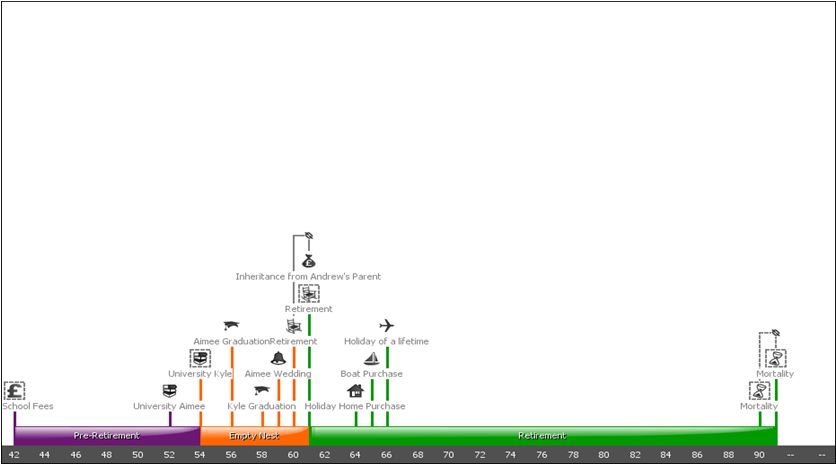

Taking into account your income, expenditure, assets, liabilities plus future planned spending or windfalls etc, we can build a visualisation of your financial future.

The initial model leads to an in-depth conversation about what is really important to you and your family’s long-term financial plans and aspirations.

This could be whether or not you are on course for that early retirement you have been striving for, or goals within your working life, a dream holiday home, funding a wedding or your children’s or grandchildren’s education.

Cash flow modelling allows us to see how achievable your ambitions are, and if so, what actions may need to be taken to make sure you are making the most of your potential.

They also help us to understand if you are able to continue to live a good life in retirement, without running out of money or even potentially dying with too much money, leaving your estate with a possible inheritance tax issue to solve.

The next step, is then to put in place actions to make the most tax efficient effective use of your money, build confidence in your plans, and also solidify our relationship as your trusted source of advice.

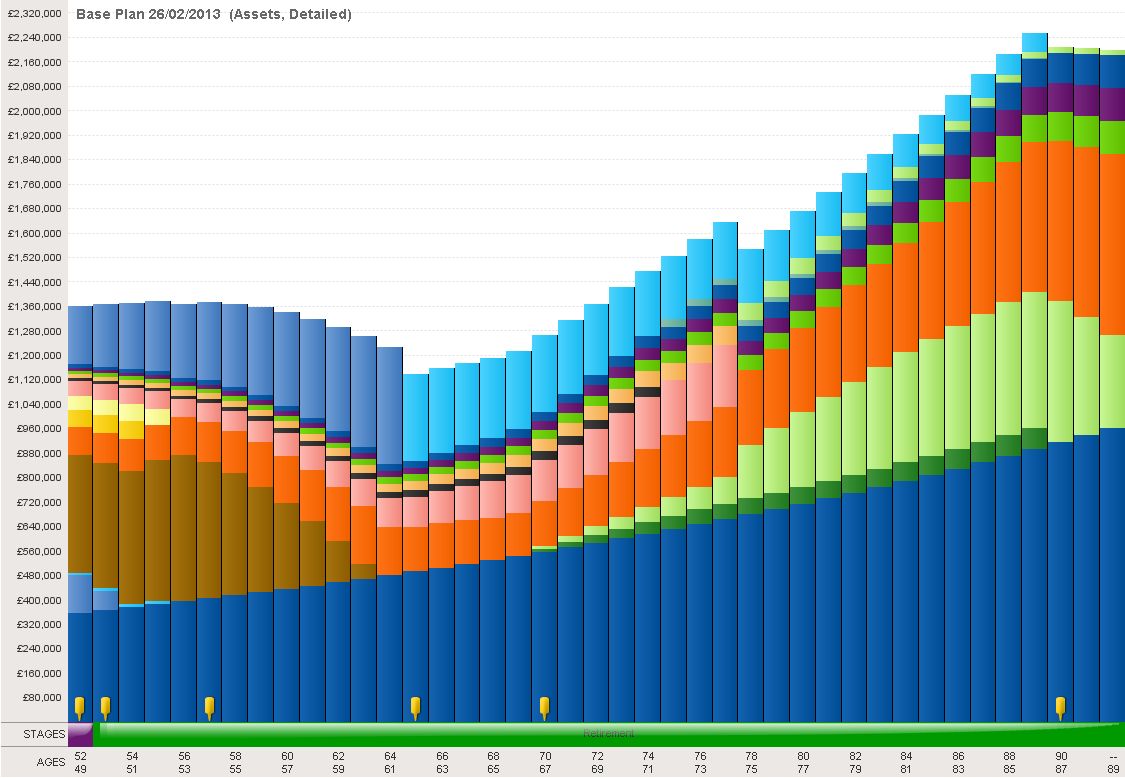

The most important part of the financial planning cash flow modelling process however, is the ongoing review.

What makes it work as an invaluable tool is revisiting the model, and re-evaluating your position on a regular basis.

Regular reviews will ensure that the course of any financial plan is maintained and is able to be followed, and amended to take into account any changes in your life.

Whether your investments have increased or reduced in value since the previous year, it’s the impact on your long-term planning that we need to consider. Annually reviewing your model helps avoid making snap investment decisions that could seriously damage long-term investment returns.

Our service is not about a single transaction.

We aim to become your trusted adviser for the long term.

By really understanding what you want to achieve with your money, for you and your families’ future, we believe we can provide the long-term advice that adds value.

Get in touch, come into our office and let us show you how we can help you by building a visual profile of your financial future.

Jonathan Beaton

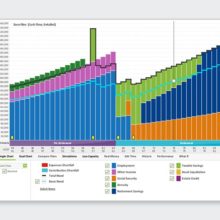

We can enter in information such as your incomes, expenses, assets and liabilities and model forward projections, such as those seen on the right.

We can enter in information such as your incomes, expenses, assets and liabilities and model forward projections, such as those seen on the right. Combining this with expert advice that guides you through an all encompassing view of your current circumstances, maybe you can generate some of your own luck.

Combining this with expert advice that guides you through an all encompassing view of your current circumstances, maybe you can generate some of your own luck.

Mindfulness is the technique of trying to catch each moment in its entirety, without the usual inner commentary or opinion we all tend to have. So it could be just reading an email calmly and carefully, without prejudging its overall contents because of a) who the sender is, or b) our opinion halfway through the message. Or it might be becoming aware of tiredness or irritation inside our mind during an important meeting (and let’s face it if it’s not an important meeting why are you having one?)

Mindfulness is the technique of trying to catch each moment in its entirety, without the usual inner commentary or opinion we all tend to have. So it could be just reading an email calmly and carefully, without prejudging its overall contents because of a) who the sender is, or b) our opinion halfway through the message. Or it might be becoming aware of tiredness or irritation inside our mind during an important meeting (and let’s face it if it’s not an important meeting why are you having one?) Our job is then to become custodian of the wealth, provide sensible investment strategies and use the tax advantages of various “wrappers” to keep the clients in the style to which they’d like to become accustomed!

Our job is then to become custodian of the wealth, provide sensible investment strategies and use the tax advantages of various “wrappers” to keep the clients in the style to which they’d like to become accustomed!